An Easy Plan to Reduce Stress and Overwhelm Around Credit Card Debt

Paying it off is as simple as following this low-tech template

Photo by Louis Hansel on Unsplash

The best way to reduce stress and overwhelm around credit card debt is to simply stop avoiding it.

No more hiding or ignoring. Quit pretending it’s not there. Bring it all out into the light so that you can be free.

In Q1 of 2022, the average American had $5,769 in credit card debt. And according to the American Bankers Association, 54% carried a balance forward.

Here’s a simple, low-tech plan of action I use with my clients for eliminating credit card debt.

Getting The Monster Off Your Back

Make a basic spreadsheet of all your bills. Label the columns as such, similar to the example below:

Date due

Company name

Minimum monthly payment

How much extra can you pay each month

Total payment each month

Current balance

Order of the cards to pay off (establishes which to focus on first)

Interest rate

Estimated pay-off date (gives you an approximate timeline)

The critical element to releasing stress, guilt, and shame around credit card debt is to put all the details on one page.

And while this step will take some work, I encourage you to fill out your spreadsheet with gusto. Dig into your most recent statements and list the current due date, monthly minimum payment, balance, and interest rate. This will help you see the big picture and develop an educated plan.

Designing The Plan

Financial experts tout two slightly different methods for paying off debt quickly.

You can focus on paying off the card with the highest interest rate.

Or, look for a quick win and pay off the lowest balance to gain momentum.

I’m all about easy and doable when tackling challenges. While it may save a few bucks to do the complicated math to figure out which card to start with and where to focus extra payments, go with your gut and do what works best for you.

Don’t get stuck in analysis paralysis. Ask yourself, Where will it feel best to make progress first? Start there and watch the magic work.

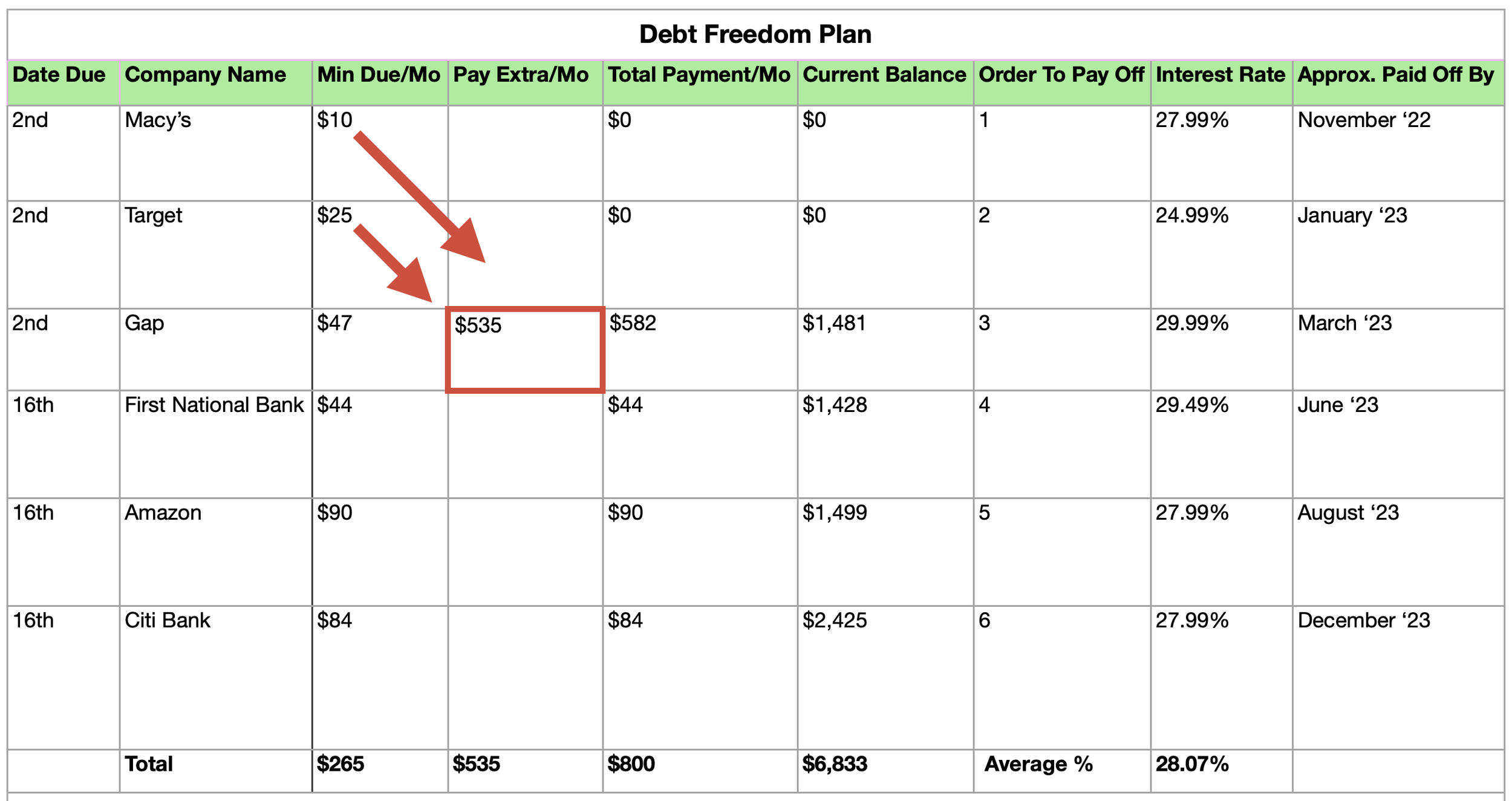

The spreadsheet is an example of a template I created for a coaching client. We developed a plan based on her current balances, interest rates, and how much she can afford to pay above the minimum payments.

Spreadsheet template that’s easy to copy and work for your specific needs.

Compounding — Interest or Time

The key to most things in life is consistency. That’s never more true than when it comes to money, whether saving it, spending it, or paying down debt.

In my client’s case, she has a handful of store credit cards and traditional bank credit cards. Unfortunately, the interest rates are all pretty high, with an average of all cards at 28.41%.

For her, we felt the best strategy was to pay off the cards in order of lowest balance first to kick start her progress, but also slightly taking into account the interest rates, as you can see in Column H with the Gap and First National Bank bills.

First, the plan is to pay the minimum on all cards. Yet, as most of us know, paying off debt quickly requires us to pay above and beyond this small monthly increment.

The second aspect is to focus on one card at a time and stretch to pay as much as possible. In this case, she can pay $500 in additional payments for a total of $800 each month dedicated to paying off debt. The high-interest rates will eat up most of her minimum payments, but the extra pop of $500 is where the real impact is made.

A Bonus Tip To Pay Off Debt Sooner

It’s important to note that we also plan to roll the financial value of the minimum amount payments forward. Meaning as one card is paid off, the minimum payment from that card is still included in the pot to pay toward the next card’s “extra payment.”

For example, in the spreadsheet, Macy’s minimum payment is $10. When this is paid off in November, her new “extra payment amount” for December will increase from $500 to $510. The Target payment for December will be the minimum of $25 plus $510 for a total of $535, which is why she’s scheduled to pay this bill off as soon as January.

When February comes around, she’ll make her minimum payment on the Gap card of $47, plus make an extra payment of $535 ($500+$10+$25=$535). See the updated example below.

When cards are paid off, move minimum payments into the “extra payment” allocation.

To keep the progress at a high level and maximize her budget, it’s essential to utilize every dollar to eliminate credit card debt. The sooner she can stop paying credit card interest, the more money she’ll save.

Freedom From Debt Stress and Overwhelm

When my client first came to me, she was fearful, ashamed, and riddled with anxiety, worry, and regret over her finances. Like many of us, she wasn’t taught about money or credit in school or by her parents.

Her #1 goal of our work together is to decrease financial fears and increase financial literacy. She wants to pay off her credit card debt, learn more about savings and retirement planning, and have enough money socked away to change careers and move to a slower-paced city within the next two years.

And while this may seem like lofty goals, we broke it down into small, bite-sized increments that aren’t necessarily easy but absolutely doable.

It’s a natural human response to avoid the things we fear most. When something is emotionally overwhelming, our brain triggers a reaction to fight, flee, freeze, or fawn.

And to add even more stress, we get stuck in mental loops of rumination, critical self-judgment, and shame.

As my client and I filled out the spreadsheet, I could literally see the emotional weight lift off her body. The mental anguish from fearfully ignoring the problem and consistently not knowing where her finances stood has been eliminated.

She feels lighter, free-er, more hopeful, and expansive. Within the next year, she’ll be debt free, and she’s absolutely ecstatic.

Like many of us, my client had to conjure the courage to be vulnerable and share the challenge with a trusted person, be open to questions and feedback, and then get to work on executing the action plan. The added benefit of an accountability partner helps hold her feet to the fire to stay consistent.

Sometimes we just need a little help to break down our fears and accomplish our goals — to be the best versions of ourselves.

Getting clear on your finances is a tremendous stress relief if you’re in credit card debt. It’s usually not hopeless or as bad as you think.

Bring your fears into the light and watch them dissipate.

. . .

Rebecca Murauskas is a high-performance Life Coach. She helps people be free of stress and overwhelm, reclaim their purpose, and feel fulfilled. Rebecca and her husband, Adam, abandoned their careers and moved to Panamá in 2019 to pursue passions for helping people heal. Take the free Time Saver Quiz and find additional content at RebeccaMurauskas.com.